Gross Margin: The Contradiction of Being Meaningless and Useful.

Gross Margin (GM) is often viewed as a simple/quick way to ascertain a company’s profitability. Our view is that it in its common form (x%), it is largely meaningless – but viewed through the right lens, it is an extremely useful measure.

Businesses use GM to indicate profitability for directly delivering the revenue generated. It is a commonly used metric to quickly ascertain a business’ relative profitability and efficiency.

The formula for Gross Margin is ostensibly simple:

Gross Margin = Revenue – Cost of Sales

Gross Margin % = Gross Margin / Revenue

GM is a non-GAAP (IFRS) measure, so the definition is not universal, but rather derived by the individual company with no external validation or audit. Although Revenue has a clear definition applicable across companies, the standardization of Cost of Sales (COS) depends very much on the industry. Companies with tangible goods typically use a standard cost measure to assign a direct cost to each Revenue generating unit so GM tends to be a fairly comparable metric across firms. However, services businesses – who must attribute personnel related expenses to revenue generating activities – have a lot more subjectivity in their calculations, particularly as people do more than billable project work.

At Bravery, we have deep P&L experience in the Professional Services category and in working with hundreds of services businesses and have encountered every conceivable construct of the GM line. We don’t put much weight on a company’s GM snapshot (say 65%) but do take seriously GM over time. Below is an outline of how our firm thinks about GM.

Cost of Sales for Professional Services

While it sounds simple enough to determine what services delivery costs belong in the Cost of Sales line, it quickly becomes subjective as classifying following costs shows:

- Billable Hours: This ought not to be controversial, any hours that directly lead to revenue should be included in the COS, whether for employees or subs.

- Non-Billable Hours: For billable staff, is all of their time assigned to COS, or just the billable hours? Or just client related hours, even if non-billable? Where is PTO, company tasks and sales support efforts assigned?

- Semi-Billable Staff: Many of the staff are part time, or have low utilization targets due to split duties. How should their time be allocated?

- Methodology or IP Development: Should this be considered SG&A? What if this is a bench project?

- Account Management: If non-billable, is this a COS or not? The effort is to support the ongoing delivery of revenue after all.

- Sales: It is Cost of Sales after all. Should commissions be included or the full amount of the sales team?

- Software Related: Should software or hosting that supports the delivery be a COS?

- Payroll Related: Are benefits, taxes, bonuses etc. included in COS?

The classification of the above scenarios is made by the individual company and consequently varies considerably. This is a perfectly acceptable state of affairs but does create the problem that Gross Margin is simultaneously a Meaningless and Useful metric.

GM is Meaningless:

That company with a GM % of 65% is not necessarily more profitable than one that is at 40%, it may well be that they have just accounted for things differently. As much as it is tempting to assume a 65% or 70% GM is impressive, in reality, it simply begs the question of what has been buried within SG&A.

Obviously at the extremes, there is information communicated in magnitude of the number (–20% vs 10% vs 90%). Typically, without some larger context, a single GM% figure is meaningless.

GM is Useful:

On the other hand, comparing a single company’s GM% over time is extremely useful. An improving GM% shows that the business is beginning to scale – which means that on average, revenue costs less to deliver. This is desirable and hints that future revenue growth will continue to lead to increasing GM% because there is some business attribute that, for a services business, means each revenue dollar requires a decreasing cost base.

Conversely, a declining GM% is concerning as it means that the business has some factor that is causing diminishing returns.

Incremental GM is Really Useful

To make GM% really useful, consider its differential or rate of change. That is to say, calculate the period over period incremental GM, which needs to be increasing per dollar of incremental Revenue. This will provide a much more forward-looking view of the business as it speaks to the incremental cost of delivering incremental revenue rather than the average cost.

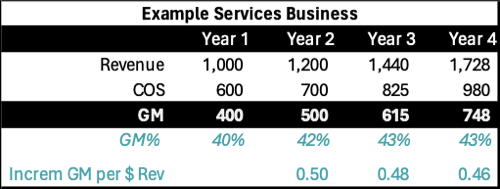

Consider the example of a hypothetical services business below:

The business is growing at 20% with a slightly improving GM% – surely a strong story. However, upon closer inspection, it is taking increasingly more spend to deliver each incremental dollar of revenue ($0.54 in Year 4) – and it is only because the incremental GM% of 46% is higher than overall GM% that the overall GM% looks healthy. This gives a far more informative picture than just the GM% level.

Best Practices

As much as there is no correct way to consider GM, the following are a few hard-earned general guidelines and best practices.

- Assuming definitions have remained consistent is not always a given (but if definitions are changing, then no measure is of any use).

- If a business is experiencing scale or diminishing returns, it is critical to really understand what drives this as it is your single best indicator of future performance. This applies equally for internal Fin-Ops and M&A practitioners.

- When selecting a Cost of Sales methodology, the golden rule is to pick a logical construct that is easy to calculate. Given that comparing between companies is meaningless, select something that you will use. For example:

- Every role (and therefore person in such role) is either COS or SG&A. All associated costs (including payroll related) flow accordingly.

- The mapping of such roles should follow a logical approach. If Account Services is a COS, that is ok as long as it stays there.

- Product or IP Development, should have a formal budget and if so, can be considered SG&A or other non-COS metrics. Otherwise, it is an informal project (i.e., a bench project) and is therefore COS.

Conclusion

Gross Margin is extremely valuable in the right context, but that doesn’t make it valuable in every context. A business’s gross margin is only good or bad in the context of its underlying definitions and its change over time.